Blog

Year of Tariff Consequences: WTO slashes 2026 trade forecast as protectionism bites

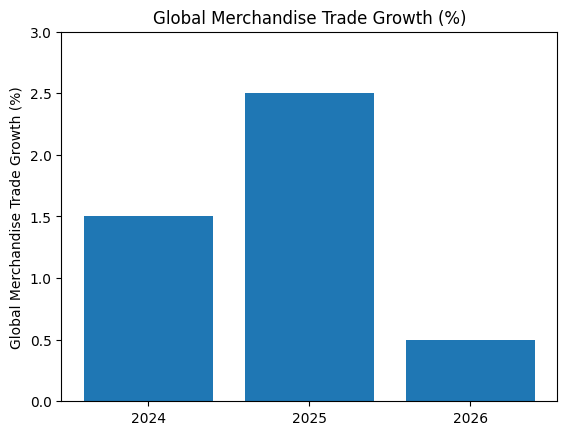

Year of Tariff Consequences has officially begun, according to a new World Trade Organization report released in the last 24 hours, warning that escalating tariffs, protectionist policies, and geopolitical fragmentation are dragging global merchandise trade toward its weakest growth in years. The WTO has sharply cut its 2026 trade growth forecast to just 0.5%, down from 2.6% growth recorded in 2025, as businesses retreat from cross-border activity amid persistent trade uncertainty.

The report marks one of the strongest warnings yet that policy-driven trade disruptions — rather than cyclical economic slowdowns — are now the dominant force shaping global commerce.

WTO’s stark warning: Why 2026 is different

The WTO’s language in the latest assessment is notably stronger than previous forecasts. Instead of temporary headwinds, the organization characterises current conditions as structural damage to the rules-based trading system.

Key messages from the WTO report

-

Global merchandise trade growth has collapsed to 0.5% for 2026

-

Protectionism, not demand weakness, is the main driver

-

Tariff uncertainty is freezing investment decisions

-

Supply chains are fragmenting into geopolitical blocs

-

Trade policy risk is now as important as inflation or interest rates

The phrase Year of Tariff Consequences reflects the WTO’s view that trade actions taken over the past three years are now converging into a measurable slowdown.

Table: Global merchandise trade growth outlook

| Year | WTO Trade Growth Estimate |

|---|---|

| 2024 | 1.8% |

| 2025 | 2.6% |

| 2026 (revised) | 0.5% |

The sharp downgrade illustrates how quickly confidence has eroded among exporters and importers.

Protectionism is now the dominant risk

Unlike previous downturns triggered by financial crises or pandemics, the Year of Tariff Consequences is being driven primarily by policy choices.

Major protectionist forces shaping 2026

-

Escalating tariff regimes among major economies

-

Sanctions-linked trade restrictions

-

Export controls on technology and minerals

-

Fragmentation of supply chains into “friendly” blocs

-

Rising use of national security clauses in trade policy

According to the WTO, businesses are no longer assuming that tariffs are temporary. Instead, they are restructuring supply chains permanently.

Graph: WTO trade growth trend (text representation)

The steep drop into 2026 highlights the shift from expansion to stagnation.

Business reaction: Pullback replaces expansion

One of the most worrying findings in the WTO report is how firms are reacting.

What companies are doing differently in 2026

-

Delaying or cancelling export expansion plans

-

Reducing long-distance sourcing

-

Renegotiating supplier contracts

-

Increasing domestic and regional procurement

-

Building inventory buffers instead of scaling trade volumes

The Year of Tariff Consequences is not only hitting volumes but altering business behaviour at a fundamental level.

Regional impact: Who is most exposed

Europe

European exporters face slowing external demand as U.S. and Asian markets impose additional trade barriers. Manufacturing-heavy economies are particularly vulnerable.

Asia

Asia’s export engines are slowing as trade routes fragment. While intraregional trade remains resilient, inter-bloc commerce is deteriorating.

North America

Tariff-driven trade policy has protected some domestic industries but raised costs across supply chains, reducing competitiveness.

Developing economies

Smaller economies are caught in the crossfire, facing reduced market access and volatile demand.

Table: Trade vulnerability by region (WTO assessment)

| Region | Exposure Level |

|---|---|

| Europe | High |

| East Asia | High |

| North America | Medium |

| Africa | Medium |

| Latin America | Medium–High |

Supply chains are no longer global — they are political

The WTO report highlights that geopolitics now outweighs efficiency in supply-chain design.

How supply chains are changing

-

Global optimisation → political alignment

-

Cost minimisation → risk minimisation

-

Single sourcing → redundant sourcing

-

Just-in-time → just-in-case

This shift is central to why the Year of Tariff Consequences is expected to have lasting effects even beyond 2026.

Critical sectors under pressure

Manufacturing

Machinery, electronics, and automotive sectors face tariff exposure across multiple markets.

Energy and commodities

Sanctions and export controls are distorting flows of energy products and critical minerals.

Technology

Export restrictions on chips and AI-related hardware are fragmenting tech supply chains.

Graph: Trade policy measures introduced globally

The cumulative effect is now fully visible in trade data.

Why 2026 is the tipping point

The WTO identifies 2026 as the year when lag effects of trade policy decisions become unavoidable.

Why the consequences are accelerating now

-

Multi-year contracts are expiring

-

Inventory built during earlier disruptions is exhausted

-

Financing costs remain elevated

-

Policy unpredictability persists

Businesses that absorbed earlier shocks are now hitting structural limits.

Inflation and consumer impact

Although tariffs are often framed as industrial policy tools, the WTO warns that they ultimately feed into consumer prices.

-

Higher import costs raise retail prices

-

Reduced competition weakens price discipline

-

Supply shortages intensify volatility

The Year of Tariff Consequences could therefore complicate inflation control efforts worldwide.

Global trade institutions under strain

The WTO report also acknowledges declining confidence in multilateral trade governance.

-

Dispute settlement mechanisms remain weakened

-

Bilateral and regional deals are overtaking global rules

-

Enforcement is increasingly selective

Without restoration of predictability, trade growth risks remaining subdued beyond 2026.

What could stabilise global trade

The WTO outlines several pathways to avoid prolonged stagnation:

Policy actions needed

-

Tariff de-escalation among major economies

-

Clearer rules on national security trade actions

-

Revitalisation of dispute resolution frameworks

-

Greater transparency in export controls

Absent these measures, the Year of Tariff Consequences may evolve into a multi-year cycle.

Table: Risks vs stabilisers for global trade

| Risk Factor | Potential Stabiliser |

|---|---|

| Tariff escalation | Negotiated reductions |

| Sanctions | Clear scope limitations |

| Export controls | Transparency mechanisms |

| Geopolitics | Regional cooperation |

Outlook for 2027 and beyond

While the WTO forecast focuses on 2026, officials caution that recovery will depend less on economic stimulus and more on political choices.

If protectionism intensifies, trade could remain close to stagnation. If cooperation resumes, growth could rebound — but rebuilding trust will take time.

Conclusion

The Year of Tariff Consequences represents a turning point for global trade. The WTO’s sharp downgrade of its 2026 forecast to 0.5% growth confirms that rising protectionism is no longer a background risk — it is the central force shaping global commerce.

As businesses pull back, supply chains fragment, and trade volumes stall, the policy decisions made in 2026 will determine whether global trade stabilises or enters a prolonged period of low growth. For governments, companies, and consumers alike, the message is clear: tariffs now carry consequences that extend far beyond borders.